This article explores how custom AI, specifically the GPT-5.4 subagent architecture, solves the most complex automation challenges in the banking sector. The hierarchical system (Orchestrator, Mini, and Nano models) guarantees bank-grade security, data isolation, and sub-100ms latency, while seamlessly integrating with legacy systems.

Introduction: The Imperative for Custom Automation in Modern Banking

In early 2026, the global financial market was shaken when a leading Wall Street investment bank announced a complete transition to a GPT-5.4 based subagent architecture. This strategic move reduced complex loan approval times by 40% and reduced compliance errors to near zero.

This event definitively proved that the era of off-the-shelf, general-purpose artificial intelligence solutions in the financial sector is over. Modern banking faces unprecedented complexity and fierce competition.

Under the dual pressure of fintech startup agility and tightening global regulations (like DORA or PSD3), traditional financial institutions must act. Custom automation is no longer just an innovation experiment; it is the only viable path to survival and market dominance.

The Problem: Limitations of Off-the-Shelf AI

General Large Language Models (LLMs) lack the deterministic accuracy required for banking processes. They are prone to hallucination, fail to meet strict data isolation requirements, and are incapable of securely communicating with decades-old, closed legacy systems (e.g., COBOL-based mainframes).

What is Custom Automation and How Does it Differ from Off-the-Shelf AI?

In the context of enterprise AI, custom automation represents an engineering approach where artificial intelligence does not operate as an external "black box" service. Instead, we build a deeply integrated system tailored to the bank's specific business logic, databases, and security protocols.

While a ready-made AI solution (like a public chatbot API) relies on general knowledge, custom-developed data processing AI agents precisely understand the bank's internal data structures. They can differentiate between the risk profile of a retail mortgage and a corporate overdraft facility.

This approach also allows for precise regulation of "Human-in-the-Loop" (HITL) processes. Custom systems not only generate responses but also directly execute transactions via deterministic API calls, all with full auditability.

The Unique Challenges of AI Adoption in the Banking Sector

For financial institutions, adopting AI is a minefield. The first and most critical hurdle is stringent regulatory compliance. Regulations like GDPR, CCPA, and local financial supervisory rules demand absolute data privacy and transparency in decision-making processes.

The second critical point is legacy system integration. The core of most large banks still runs on decades-old, monolithic architectures. A modern AI system must be able to communicate securely with these systems via middleware layers without compromising stability.

Finally, there is the requirement for extreme accuracy and low latency. In an algorithmic trading platform or a real-time fraud detection system, an error or slow response time can cost millions. There is no room for AI "creativity" here.

Introducing the GPT-5.4 Subagent Architecture: A Paradigm Shift in Banking AI

The solution to these complex challenges is the GPT-5.4 subagent architecture. This is not a single massive, omniscient model, but an intelligent, distributed network. This approach radically transforms the concept of Agentic OS and custom automation in an enterprise environment.

The foundation of the system is an evolution of the "Mixture of Experts" (MoE) topology, where tasks are distributed not within the network, but among dedicated, separate AI entities. This drastically reduces computational overhead and increases security.

Technical Deep Dive: The Subagent Architecture

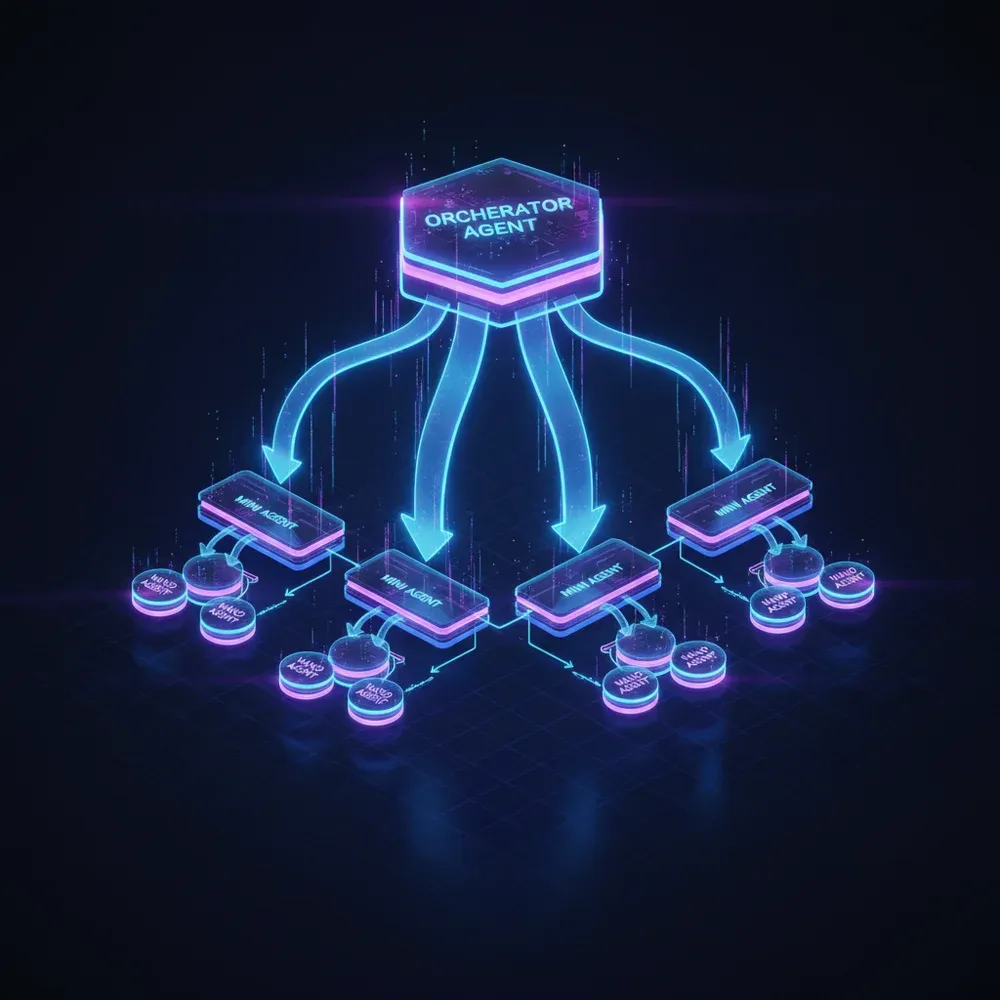

The system consists of a central 'Orchestrator' model that understands user intent and breaks the task down into microservices. It assigns these subtasks to specialized 'Mini' and 'Nano' models, which execute requests in parallel, and the Orchestrator then synthesizes the result.

Hierarchical Intelligence: The Role of Mini and Nano Models

At the top of the hierarchy is the GPT-5.4 Orchestrator. This model does not need a deep understanding of banking database SQL syntax. Its job is context understanding and routing. When a customer requests a credit limit increase, the Orchestrator activates the appropriate subagents.

The 'Mini' models (e.g., 7B-13B parameter models fine-tuned on specific data) are responsible for more complex subtasks, such as risk analysis or processing text documents (like proof of employment). These models run in strictly isolated environments.

The 'Nano' models (under 1B parameters, often quantized to INT4 precision) perform the smallest, deterministic tasks. For example, a Nano agent's sole task might be to construct and validate the JSON payload of a specific API call. These execute in milliseconds.

Orchestration and Specialization: How Subagents Collaborate

Communication between subagents occurs via strictly typed protocols. They do not "chat" with each other in plain text; instead, they exchange structured data objects (like Pydantic models). This guarantees that data is not distorted along the chain.

This specialization also enables error isolation. If the document-processing Mini agent encounters an error, it does not crash the entire system. The Orchestrator can retry or escalate the issue to a human operator while other processes continue to run smoothly.

Achieving Bank-Grade Security and Compliance with Subagents

The biggest fear for banking IT leaders is data security. With traditional LLMs, there is a risk that the model "learns" sensitive customer data and later outputs it in response to another prompt. We detailed this risk in our article on the security risks of data processing AI agents.

The GPT-5.4 subagent architecture solves this problem through the hardware and software-level integration of Zero Trust and Privacy by Design principles. Data never leaves the bank's secure perimeter.

Data Isolation and Privacy by Design

In the system, data isolation is implemented at both physical and logical levels. The central Orchestrator model only receives anonymized, masked data (e.g., Customer_ID_12345). Real, sensitive data (PII - Personally Identifiable Information) is only accessed by the lowest-level Nano agents running in a strictly closed network.

When a Nano agent queries an account balance, it executes the operation on the bank's own on-premise or private cloud infrastructure. It sends the result back up the chain aggregated, with sensitive details removed, so higher-level models never encounter raw customer data.

Auditability and Regulatory Adherence

Financial regulators require explainability in decision-making (Explainable AI - XAI). If a loan application is rejected by AI, the bank must know exactly why. With a monolithic LLM, this is nearly impossible.

The subagent architecture, however, records every single step, API call, and intermediate result in an immutable audit log. Compliance Checker Nano agents continuously monitor transactions and immediately block the process before execution if they detect any regulatory anomaly.

Unlocking Ultra-Low Latency: The Key to Real-Time Financial Services

Modern banking is real-time. When authorizing a card transaction, the fraud detection system must make a decision in milliseconds. The 1-3 second response time of traditional cloud-based LLM APIs is unacceptable here.

The GPT-5.4 architecture achieves sub-100ms latency by decentralizing tasks and optimizing models. This speed allows AI to be not just an assistant, but an active, real-time component of critical infrastructure.

Optimized Processing with Specialized Agents

The secret to speed is specialization. A general model must process billions of parameters for every single request. In contrast, a Nano agent trained exclusively to validate transaction codes works with only a few million parameters.

These small models run directly in-memory, often on custom AI accelerator chips (ASICs) or optimized GPUs. Because tasks run in parallel, the total processing time is not the sum of all tasks, but the time of the longest subtask.

Scalability and Performance Under Load

During Black Friday or a market panic, transaction volumes skyrocket. The system must maintain response times even then. The subagent architecture runs in a cloud-native and containerized (Kubernetes) environment.

This means if the fraud detection Nano agents become overloaded, the system automatically spins up new instances of them in a fraction of a second, without needing to scale the entire Orchestrator model. This is not only fast but highly cost-effective.

Real-World Applications: AI Account Managers and Automating Complex Financial Workflows

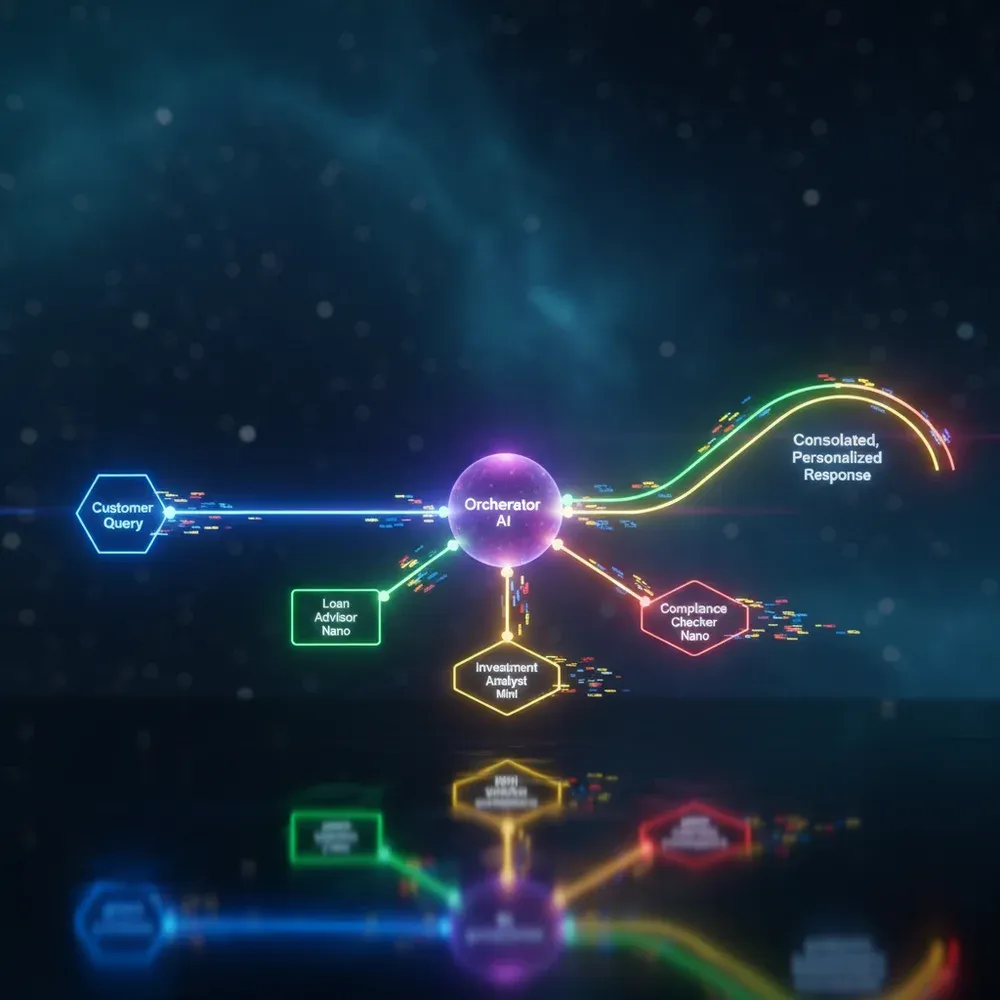

The true value of the technology is revealed in real-world business applications. Imagine a personalized AI account manager available 24/7. This is not a simple FAQ chatbot, but an advanced RAG (Retrieval-Augmented Generation) based AI chatbot that knows the customer's entire financial history.

When a customer asks for investment advice, the Orchestrator engages the Portfolio Analyst Mini agent, which analyzes real-time market data and the customer's risk tolerance. Meanwhile, a Compliance Nano agent checks if the proposed portfolio complies with MiFID II guidelines.

In loan processing, the system can automatically gather data from credit bureaus, analyze bank statements (using OCR and NLP), and provide pre-approval in seconds. This level of automation reduces turnaround time from weeks to minutes.

Ready to revolutionize your banking processes?

Don't fall behind the competition. AiSolve's expert team helps design and implement the most advanced GPT-5.4 based custom automation systems.

Request a Free Consultation

Implementation Strategy: From Concept to Deployment

Deploying such a robust system cannot happen overnight. It requires a well-structured, phased implementation strategy that minimizes risks and maximizes Return on Investment (ROI).

The process always begins with an in-depth analysis of the existing infrastructure and business processes. The goal is not to automate everything immediately, but to find the bottlenecks where AI can create the most value.

Needs Assessment and Data Infrastructure Preparation

The first step is dismantling data silos. AI agents are only as good as the data behind them. Banking databases (SQL, NoSQL, data warehouses) must be made accessible to the models through a unified, secure Data Fabric layer.

This is followed by process mapping. We determine which tasks a Nano agent can perform autonomously and where "Human-in-the-Loop" approval is required. In this phase, we also establish strict Role-Based Access Control (RBAC) and privacy rules.

Phased Rollout and Continuous Optimization

Deployment always starts with a narrowly focused Pilot project (Proof of Concept - PoC). For example, automating internal IT helpdesk processes or pre-screening retail loan applications. This allows for system fine-tuning in a real but low-risk environment.

After a successful Pilot comes the scale-out phase. The system continuously learns from its own operations (Reinforcement Learning from Human Feedback - RLHF). Based on operator feedback, the subagents become increasingly accurate and efficient.

The Future of Banking: Competitive Advantage Through Custom AI Solutions

Financial institutions that recognize the potential of custom automation will gain an insurmountable competitive advantage. Alongside a drastic reduction in operational costs, the primary benefit is the revolutionization of User Experience (UX).

The bank of the future is proactive. AI agents don't just respond to customer requests; they anticipate their needs. If an unusually large sum appears on a customer's checking account, the AI can immediately offer personalized investment options before the customer turns to a competitor.

This agility allows banks to compete with the most innovative fintech companies while maintaining the stability and trust characteristic of traditional financial institutions.

Partnering for Success: How to Build Your Custom AI Solution

Building a GPT-5.4 level subagent architecture is not an average IT project. It requires deep AI engineering knowledge, cybersecurity expertise, and an intimate understanding of financial processes. Therefore, choosing the right technology partner is critical.

At AiSolve, we don't sell boxed software. We design, build, and operate custom automation solutions that perfectly fit your company's DNA. Our experts guide you through the process from the initial strategic workshops to full scaling.

Step to the Forefront of Financial Innovation

Speak with our experts and discover how to transform your banking processes with the power of AI. Book a free, no-obligation technical consultation.

Book a ConsultationConclusion: Embracing the Era of Intelligent Financial Automation

The emergence of the GPT-5.4 subagent architecture is a watershed moment in the financial sector. It allows banks to finally bridge the gap between strict security requirements and the efficiency offered by state-of-the-art AI technologies.

Through custom automation, financial institutions can not only replace manual, repetitive tasks but also create intelligent, real-time decision-making systems. This technology reduces risks, optimizes resources, and elevates customer service to a new level.

The question is no longer whether AI will transform banking, but whether your company will be at the forefront of this revolution or fall behind competitors. The era of intelligent financial automation has begun.

Frequently Asked Questions (FAQ)

What is the cost of developing a custom AI automation solution in a banking environment?

Costs depend heavily on project complexity, the number of legacy systems to integrate, and the state of the data infrastructure. A smaller PoC (Proof of Concept) project automating a specific process can start from a few million forints, while deploying a full, bank-grade GPT-5.4 subagent architecture may require an investment of tens of millions. However, it is important to note that these systems often pay for themselves (ROI) within 6-12 months through drastic reductions in operational costs.

What is the average implementation time for deploying a GPT-5.4 based subagent system?

A targeted Pilot project (PoC) can go live in as little as 4-6 weeks using AiSolve's agile methodology. Implementing a comprehensive system affecting multiple departments and complex workflows, which includes in-depth data security audits and legacy system integration, typically takes 3-6 months. The phased rollout ensures that the bank realizes measurable business value within the first few months.

How does custom automation ensure compatibility with existing banking legacy systems?

Custom AI systems do not attempt to replace existing core banking systems (e.g., monolithic mainframes). Instead, we build an intelligent middleware layer and custom API gateways. Nano agents can communicate using the specific protocols used by older systems (whether SOAP, XML, or custom TCP/IP messages), allowing the AI to integrate seamlessly without modifying the critical backend systems.

What are the data requirements for implementing such an advanced AI system?

The advantage of GPT-5.4 subagents is that they do not require massive, retrained datasets from scratch. The models already possess fundamental logical capabilities. The bank needs to provide structured (SQL databases, transaction logs) and unstructured (policies, customer service emails, PDF documents) data to populate RAG (Retrieval-Augmented Generation) vector databases. The most important factor is data quality and cleanliness, not necessarily quantity.

How does the GPT-5.4 subagent architecture differ from traditional large language model (LLM) applications in banking?

Traditional LLMs (like public ChatGPT) attempt to solve every task as a single, massive model, which is slow, expensive, and poses security risks (hallucination, data leakage). The GPT-5.4 subagent architecture is decentralized: a central Orchestrator model directs tasks to tiny, specialized (Mini and Nano) models. This hierarchy guarantees sub-100ms latency, deterministic accuracy, and strict data isolation, which is essential for banking compliance.

What measurable ROI can be expected from implementing custom AI automation?

Measurable ROI appears immediately across multiple areas. By automating back-office processes (e.g., loan approval, KYC/AML checks, document processing), manual labor hours can be reduced by an average of 40-60%. With the introduction of AI account managers, customer service costs drop drastically while customer satisfaction (NPS) rises due to 24/7, instant, and personalized service. Furthermore, minimizing error rates can save the bank from significant compliance fines.

Készen állsz a saját weboldaladra?

Ingyenes konzultáció során átbeszéljük, hogyan segíthetünk vállalkozásodnak növekedni egy modern, gyors és konverzióoptimalizált weboldallal. 14 nap alatt kész, 0 Ft induló költséggel.